Section 86 Estate Freeze | Section 85 Rollover | Minimize Your Tax Obligations

Paying taxes later and less of them is always a good thing. Thankfully, there are several provisions under the Income Tax Act that allow you to creatively freeze your assets at their current value and defer paying taxes to a later date. Let’s look at two of these: the Section 85 Rollover and the Section 86 Estate Freeze.

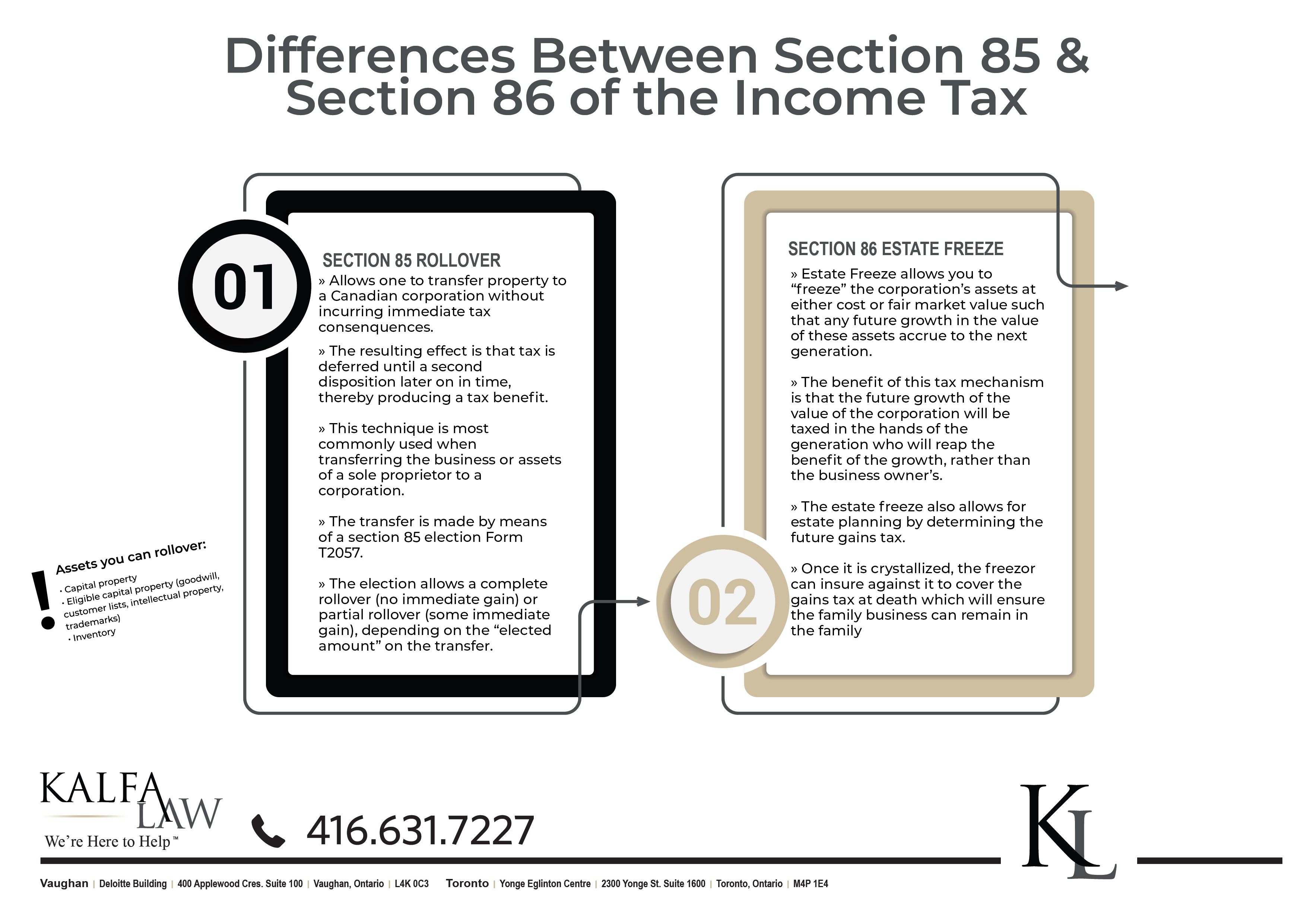

The section 85 Rollover is a tax saving tool that allows you to transfer property to a Canadian corporation without incurring immediate tax consequences. An Estate Freeze allows you to “freeze” the corporation’s assets at either cost or fair market value so that any future growth in the value of these assets accrues to the next generation.

The resulting benefit of the former is that tax is deferred until a second disposition later on in time, thereby producing a tax benefit. The benefit of the latter is that the future growth of the value of the corporation will be taxed in the hands of the generation who will reap the benefit of the growth, rather than the business owner’s.

Section 85 Rollover

Section 85 of the Income Tax Act (the “Act”) allows one to transfer property to a Canadian corporation without incurring immediate tax consequences. This technique is most commonly used when transferring the business or assets of a sole proprietor to a corporation. As a corporation is a separate legal entity, when an individual transfers an asset (say, their tools and machines) to the corporation, this triggers a tax, as there is a disposition of the asset by the sole proprietor. A section 85 rollover is essentially a tool to neutralize the tax on the transfer and defer the payment of the gains tax until a second disposition at a later date.

The transfer is often called a “rollover,” because it is transferred at cost or fair market value, thereby avoiding the immediate recognition of accrued gains.

The transfer is made by means of a section 85 election Form T2057. The election allows a complete rollover (no immediate gain) or partial rollover (some immediate gain), depending on the “elected amount” on the transfer.

In order to qualify for the election as consideration for the transfer of the property, you must retain at least one share in the corporation. You may also retain non-share consideration—often called “boot” — although the boot may affect your elected amount in the manner discussed below.

What assets can you rollover?

The following can be transferred using section 85(1):

Capital Property:

Capital property that increases in value through favourable market conditions and any other property that, upon its disposition, will result in capital gains.

For example, Jane purchased land for $100,000 in 2005. It is now worth $1,000,000. Although there is a profit of $900,000 on the asset, using the rollover, Jane can transfer the property to a corporation at its cost of $100,000.

Eligible Capital Property

Eligible Capital Property refers to intangible assets, including goodwill, customer lists, intellectual property, trademarks etc.

Inventory

Inventory refers to assets that have increased in value from its initial purchase amount.

When Should You File an Election?

The election must be filed by the earlier of your or your corporation’s tax return due date for the taxation year in which the transfer took place. Late filing within three years of that day is allowed, subject to a penalty. After the three years, you may be able to file late if the Canada Revenue Agency (CRA) is of the opinion that it would be “just and equitable” to allow the late filing. Again, a penalty will apply.

Section 86 Estate Freeze

The primary purpose of an estate freeze is to establish all or part of the value of growing assets at their current fair market value, such that any future growth in the value of these assets accrues to the next generation. The resulting effect is that the value of the asset’s future growth will not be taxed in the hands of the current shareholder at the time of sale or his/her death.

In a section 86 estate freeze, the shareholder causes the corporation to undertake a capital reorganization. The shareholder gives up all of the common shares to the business in return for preferred shares using Section 86 of the Income Tax Act by exchanging the class of shares. By using this provision of the Act, the freezor freezes his or her value of shares in fixed-value preference shares. In turn, the next generation subscribes for common shares, which reflect the continued and future growth of the corporation and its value.

Benefit of the 86 Estate Freeze

If shareholder had held on to his common shares, he would pay an enormous amount of gains tax upon his eventual death. Since a good portion of the benefit of the wealth will devolve onto the shareholder’s children, the estate freeze allows the children to pay the gains tax on their portion of wealth or value inherited.

The estate freeze also allows for estate planning by determining the future gains tax. If no estate freeze is undertaken, at the eventual death of the business owner, there is a deemed disposition of shares and a gains tax is triggered. If an insurance policy was not previously taken out, the family of the deceased will have to pay the gains tax. If the business was profitable, the gains may be large. If the family does not have the liquidity to pay the gains tax, they may be forced to sell the business in order to satisfy the tax bill. By undertaking an estate freeze, the freezor is able to calculate the future gains tax and freeze it. Once it is crystalized, the freezor can insure against it so that the family has the funds to pay the gains tax on the owner’s eventual death and the family business can remain in the family.

Whichever tax saving tool you use, make sure you understand the benefits and drawbacks of each. Consult a tax lawyer at Kalfa Law Firm regarding these tax planning techniques to ensure that you maximize these tools while minimizing your tax obligations.

-Shira Kalfa, BA, JD, Partner and Founder

Shira Kalfa is the founding partner of Kalfa Law Firm. Shira’s practice is focused in corporate-commercial and tax law including corporate reorganizations, corporate restructuring, mergers and acquisitions, commercial financing, secured lending and transactional law. Shira graduated from York University achieving the highest academic accolade of Summa Cum Laude in 2012. She graduated from Western Law in 2015, with a specialization in business law. Shira is licensed to practice by the Law Society of Ontario. She is also a member of the Ontario Bar Association, the Canadian Tax Foundation, Women’s Law Association of Ontario, and the Toronto Jewish Law Society.

© Kalfa Law Firm 2020