Income Sprinkling Canada: Tax Savings Through Income Sprinkling

We are now a full year into the Canadian government’s new rules for income sprinkling in Canada using private corporations, whereby income can no longer be “sprinkled” among various family members in order to reduce the tax bracket of the higher earner.

In the article Income Splitting Canada: New Income Splitting Rules (TOSI), you can learn more in depth about income splitting in Canada, otherwise known as “income sprinkling” and the CRA rules, in greater detail and the exceptions to the new rules.

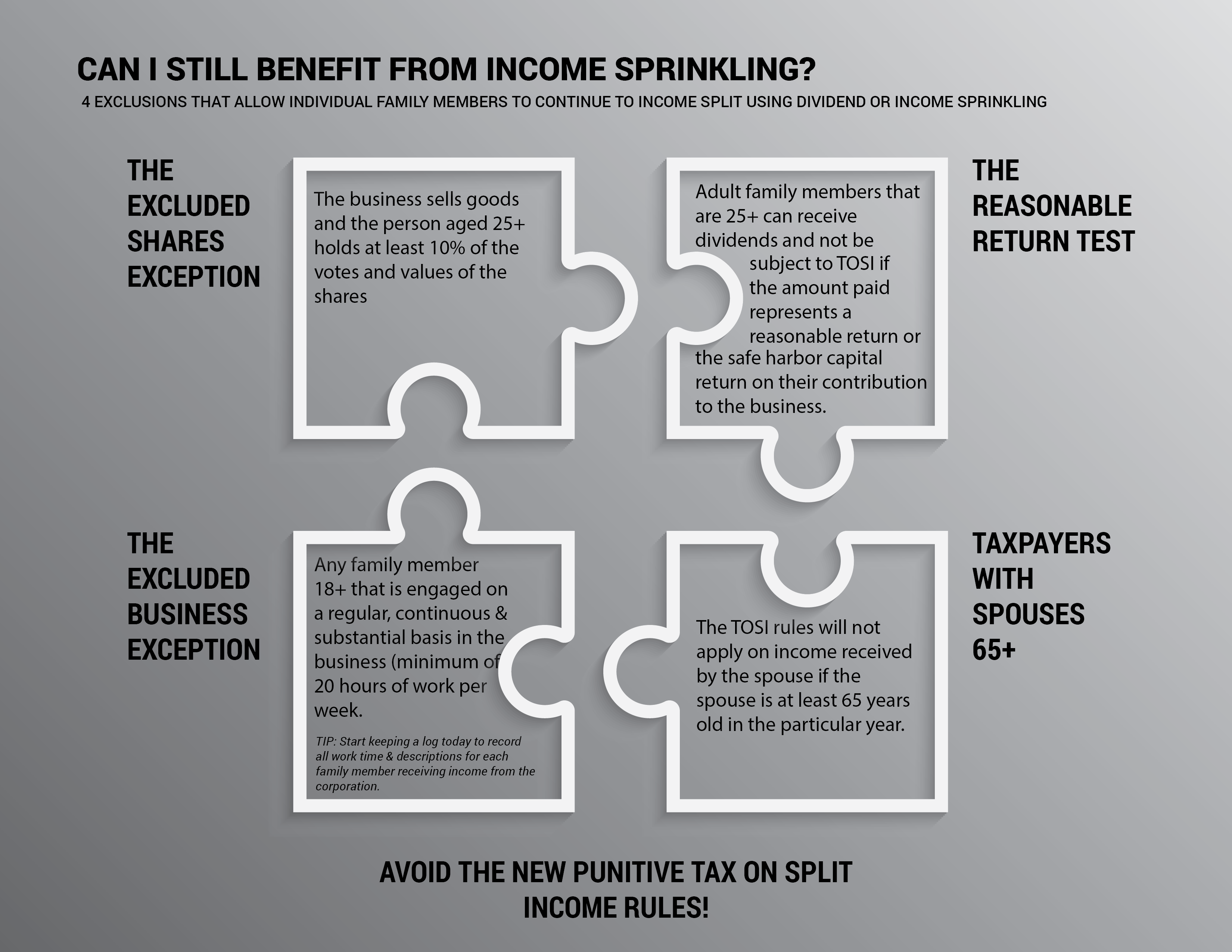

In summary, income can be “sprinkled” or split with other family members, as long as you can prove the following:

- The family member is over the age of 18 and has worked at least 20 hours a week in the present year or in 5 non-cumulative preceding years.

- The family member is over the age of 25 and owns more than 10% of the votes and value of the shares of corporation directly (not through a trust) and the business is not in the provision of services, and the corporation is not a professional corporation.

- The family member is over the age of 25 and the income represents a reasonable return or safe harbor capital return on his or her investment.

- The family member is over the age of 65.

Aside from the above, there are some other tax-income sprinkling ideas allowed by the CRA that can help you save money aside from traditional income splitting:

A. Pension Income Sprinkling

Seniors can split their pension income with their spouse or partner including income that qualifies for the federal pension income credit. This would allow higher earners to split up to 50% of their pension income when it is withdrawn at the age of 65 or older from an employer-sponsored registered pension plan or a registered retirement income fund (RRIF).

A higher earning spouse can also take out a spousal RRSP, whereby the spouse earning less income pays taxes at a reduced tax bracket in the year the money is withdrawn. Bonus: the higher income spouse can claim the contribution as a deduction.

B. Spousal income sprinkling

Loaning money to a spouse or partner who is earning less provides another opportunity to achieve tax savings. The money must be loaned at a 2% interest rate for the purpose of making an investment. The investment returns are then taxed at the lower earner’s marginal tax bracket. The interest on the loan must be paid by January 30 annually for the prior year’s income to maintain the income splitting advantages. Bonus: the prescribed interest rate of 2% continues for the duration of the loan, which can be for many years or even decades.

Alternatively, if you don’t want to collect interest from your spouse on a loan, you can avoid attribution rules by taking the money your spouse earned through an investment and placing it in another investment account. This “second-generation” income will be taxed at the lower income spouse’s rate.

The higher income spouse can also save taxes by paying for all the expenses, thus freeing up income for the lower income spouse to invest. The money earned by the lower income spouse will be taxed at a lower rate.

Finally, you can swap income-producing assets for your lower income spouse’s (or other family member’s) non-income producing assets of equal value, say jewelry or your spouse’s share of the house as long as he or she paid for it. The lower income spouse will pay taxes on the income-producing asset at a lower tax rate.

C. Income sprinkling with children

Similar to the strategy discussed above, you can set up a trust fund in your children’s name as long as they are under 18 years of age. The money loaned to the trust is payable at the prescribed 1% rate of interest. The trust invests the funds and the capital gains (not dividends or interest) earned will typically be shielded from tax.

If you own a corporation, you can take advantage of yet another strategy for tax savings. You can loan money to your adult child who is a student. Your child will pay little or no tax on it if he or she has little income. When your child graduates and begins to earn an income, he or she is entitled to a deduction for the money that is paid back.

FAQ’s:

Contact a Lawyer

While traditional income sprinkling opportunities in Canada were fundamentally changed and largely eradicated by the overhaul to corporate tax planning by the Liberal government in 2017, some formidable tax planning opportunities are still available to Canadians.

Contact Kalfa Law Firm to speak with one of our tax and corporate lawyers regarding creative ways we can minimize your tax obligations.

-Shira Kalfa, BA, JD, Partner and Founder

Shira Kalfa is the founding partner of Kalfa Law Firm. Shira’s practice is focused in corporate-commercial and tax law including corporate reorganizations, corporate restructuring, mergers and acquisitions, commercial financing, secured lending and transactional law. Shira graduated from York University achieving the highest academic accolade of Summa Cum Laude in 2012. She graduated from Western Law in 2015, with a specialization in business law. Shira is licensed to practice by the Law Society of Ontario. She is also a member of the Ontario Bar Association, the Canadian Tax Foundation, Women’s Law Association of Ontario, and the Toronto Jewish Law Society.

© Kalfa Law Firm 2020